Mark: Welcome to unsuitable on Rea Radio, the award-winning financial services and business advisory show that challenges your old-school business practices, and the traditional business-suit culture. On the show, you’ll hear from industry professionals who will challenge you to think beyond the suit and tie, who will offer you meaningful, modern solutions to help you enhance your company’s growth. I’m your host, Mark Van Benschoten. I know I’m not the only parent out there who wants the best for their kids, but parenting can wreak havoc onto your bank account. Whew!

I have three daughters of my own, as I pause and gasp for air, and the amount of money they cost me, the money I’ve invested in them over the years is mind-blowing. Olivia, Victoria, and Eva, I would do it again in a heartbeat, but what if I told you there’s a way that your kids can actually save you some money? Yeah, you heard that right. They could save you some money. Today, on unsuitable on Rea Radio, Ashley Matthews, a tax manager here at Rea, and mother of three, is going to educate us on the ways our kids can help us soften the tax blow. After all, they’ve earned the title “the world’s cutest tax deduction” for a reason. Welcome to unsuitable, Ashley.

Ashley: Thanks. Good to be here.

Mark: Where were you 20 years ago, is what I want to know.

Ashley: 20 years ago, probably middle school.

Mark: Middle school.

Ashley: Yeah.

Mark: Well, now that I feel old and humbled, but so my daughters currently are 20, 19, and 12 …

Ashley: OK.

Mark: … and so the 20 and 19 years old are in school.

Ashley: Great.

Mark: There’s a heavy, heavy burden there. Again, girls. I’m not sure they listen to this, so I’m not sure why I’m falling all over them, but if they do, obviously there is an investment there, and we want the best for our kids, so what’s the golden goose there?

Ashley: There are quite a bit of tax incentives, related to college especially. The IRS has made it quite easy to … They’re incentivizing parents to save for college, and so there are quite a few credits and saving opportunities that will save you money on taxes.

Mark: Are they easy? Are they hard?

Ashley: Well, that’s a …

Mark: As you chuckle, you mean this …

Ashley: … really good question.

Mark: That’s my second one today.

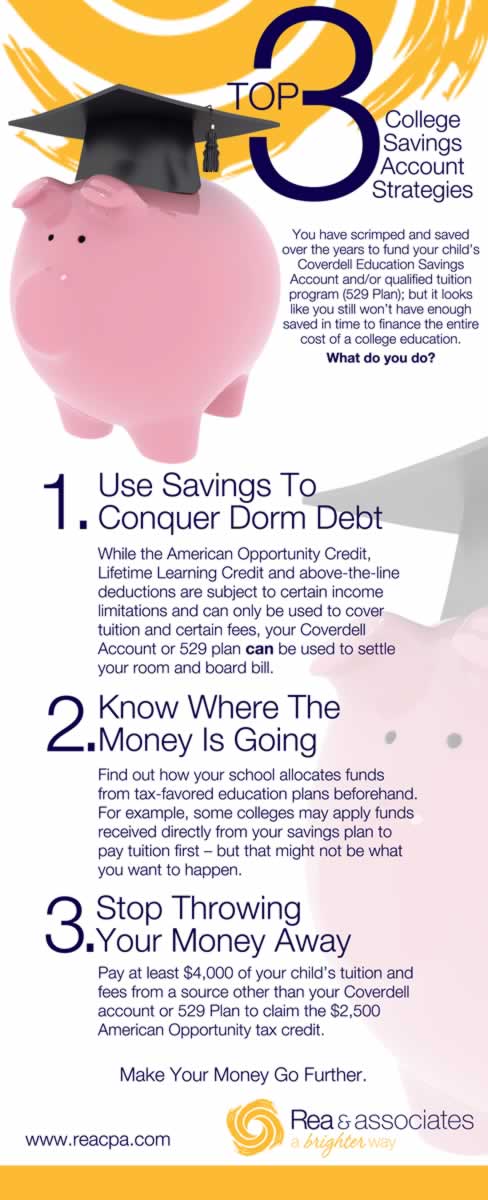

Ashley: There is, it’s a little bit of a puzzle when you’re looking at what to take advantage of when you have children in college. There’s two different credits. There’s the American Opportunity Credit, and there’s a Lifetime Learning Credit, and they are both credits towards college, post-secondary education, but they have a little bit different requirements, and different ways to take advantage of them, and one may be more advantageous than the other, and they also have different phase-out amounts, so depending on the income level of the parents, that would be claiming the deduction. It may be, make more sense to claim one versus the other.

Mark: Sounds complicated.

Ashley: It is, and then on top of that, there is an opportunity to deduct tuition and fees, and you can’t take all of it together, and so it is a little bit of a puzzle, where we can definitely help run those numbers and figure out where you can get the best savings related to the college expenses.

Mark: Does any of this have to do with the FAFSA form? Do we need to fill out the FAFSA form for all this?

Ashley: You don’t have to fill out the FAFSA form for any of this, so this really relates to any expenses that you’re coming out of pocket to the college, books and supplies, room and board, so anything that you’re paying out of your pocket. It doesn’t relate, at all, to any scholarships you’re receiving, those are tax-free, which is great, or any federal financial aid that you receive, typically, that’s tax-free as well.

Mark: I don’t know if you had a chance to listen to Kaitlin’s podcast, but she talked about her personal experience of helping somebody fill out the FAFSA form, and that was just inspiring.

Ashley: Oh, I’m sure it was inspiring that …

Mark: I don’t know if you’ve heard that podcast or not yet.

Ashley: No, no. No, I haven’t.

Mark: You haven’t? You have to get back and listen to that.

Ashley: I will.

Mark: Then that’s for college, for college, somebody who’s currently in college. What should we be doing with our, my children are a little … Than your children …

Ashley: Right.

Mark: … what should I have done that hopefully you’re doing now?

Ashley: Great question, so there are a couple different opportunities for saving for college that allow you to put the money in now, or my children are 6, 4, and one, so for me …

Mark: Wow.

Ashley: … put the money in now, and when I take the money out, in 10, 15 years … Yeah.

Mark: Sounds like it’s a long way away, but it’s really, really not, trust me.

Ashley: Yeah, I know. I know. The growth is tax-free if you use it on qualified expenses, which are typically actual tuition books and supplies, room and board, depending upon what particular savings plan you use. Sometimes computer equipment, laptop, stuff like that, can be a qualified expense as well. The nice thing about that is, for most of the savings plan, I’m sure everybody’s heard the 529 savings plans, 529 savings plans, thrown around there. That’s the most common. A lot of states will give some type of a deduction for contributions into a 529 plan in the year of contribution, so Ohio is a great state that does that. On your Ohio personal income tax return, they allow for a deduction of $2,000 per child, so if you put $2,000 a year in your child’s 529 plan, they’ll allow you to deduct $2,000 per child.

Mark: Is there any requirement that the child attends school in that state?

Ashley: Nope, and it’s just that you have to invest in the state sponsor plan, so Ohio has a state sponsor 529 plan, and as long as you invest in that plan, you can take advantage of the deduction.

Mark: This is getting to be personal, and so I invest into that plan, and I take the money out, and my child does not to go to school in-state. Is there an issue there? No. Phew. Thank you.

Ashley: No. No issue there.

Mark: I can relax.

Ashley: The nice thing is, that’s not just parents, so grandparents set up that type of plan in their grandchild’s name, and sets it up in their niece or nephew’s name, they’re entitled to the deduction as well, and it carries over, so if you contribute $6,000 one year and nothing the next, you can carry over that unused deduction to deduct it in future years.

Mark: The next year you can add that 6 to the other 6?

Ashley: Next year, so you would get 2,000 a year, so if I contribute 6 in year 1, I get to take 20,000 of that as a deduction, 4,000 carries over …

Mark: OK.

Ashley: … and so if I did contribute nothing in year 2, which I don’t recommend, but if you contribute nothing in year 2, you could pull from that $4,000 carryover that you have to get your $2,000 deduction, so it’s kind of cumulative.

Mark: Is there, I don’t contribute anything in 2016. In 2017, can I contribute 4,000, or I could just do the 2,000?

Ashley: Well, you can contribute as much as you want, but you’re only going to get the $2,000 deduction. That’s the maximum, in a year of contribution. There’s no carryover if you don’t take advantage of the deduction in the past.

Mark: If I put in 6 in 2016, I can … Okay, I can carry that over. Again, complicated.

Ashley: I can see the wheels turning.

Mark: Yeah. I’m thinking.

Ashley: You’re thinking on your own situations, huh?

Mark: I think we need to cut this short on …

Ashley: Mark needs to go look at his tax returns.

Mark: Correct. Make sure it’s still in the period of, we can amend that.

Ashley: There you go.

Mark: What else, anything else that you would recommend from being a parent of [your kid 00:07:52]?

Ashley: Definitely, definitely. I’m sure everybody’s heard of the healthcare flexible spending accounts, where, through your employer, you can put in up to $5,000 pre-tax, take those out, if you paid for qualified medical expenditures, that is tax-free. There is also an account exactly like that, but for dependent care expenses, that most people don’t know about, so if you are married, it’s $5,000, single it’s $2,500, per family. You can put, set that money aside tax-free through a cafeteria plan at work, and as long as you use it to pay qualified dependent care expenses, it’s tax-free.

Mark: It’s pre-tax money.

Ashley: Mm-hmm (affirmative).

Mark: Does the employer have to have that set up? Is that something the employee can insist on?

Ashley: The employer has to have the plan set up, but most employers that have a healthcare flexible plan …

Mark: Also have a dependent …

Ashley: … also have a dependent care plan.

Mark: That’s $5,000?

Ashley: Yes.

Mark: For married.

Ashley: Married, and $2,500 for single, yes.

Mark: Any talk of movement of those amounts? Are those amounts pretty solid?

Ashley: Those amounts are pretty solid. There hasn’t been much talk of movement of those amounts. It would be nice to index those for inflation, but they’ve been pretty solid for a good amount of time, and it’s good to say, too, that qualified expenses are daycare, of course, but sometimes day camps, so during the summer, day camps can qualify, preschool qualifies. It’s, the typical definition are expenses that are paid for childcare while the parent is working or looking for work.

Mark: Is there a requirement that both parents work?

Ashley: Not necessarily. It depends on the situation, but there could be an opportunity where one parent is steady, working out of the home, the other parent maybe doing part-time work or something like that, but you just have to look at every situation.

Mark: Does not have to be full-time employment …

Ashley: Correct.

Mark: … for both parents.

Ashley: Correct.

Mark: Is there a situation where you might have a thirteen-year-old, twelve-year-old child, where you might employ them in a business? Is there a potential for that? Is there any issues with that?

Ashley: Well, a 12 or 13-year-old, I think you have probably labor law issues.

Mark: OK. I will get through those, OK.

Ashley: Sorry. There are opportunities …

Mark: Sorry, yeah?

Ashley: … for families who own their own business to employ their child and pay them a wage. There’s certain requirements for that, but, yeah, I mean, that’s an opportunity.

Mark: Assuming they’re providing services to-

Ashley: Exactly, yes, they have to actually be working.

Mark: Doing something.

Ashley: Yes, but yeah, if you have a family business, and your child is providing services, there’s opportunity there, so …

Mark: For them to be paid, and …

Ashley: Exactly, and obviously the business would deduct that as a wage.

Mark: Pick it up, and the child will have to …

Ashley: Take it off his income.

Mark: … pick it off his income.

Ashley: Correct. Correct. One thing I didn’t mention, going back to kind of the dependent care, there’s also a credit that you can take on your tax return for dependent care expenses, and you can actually qualify to do the pre-tax dependent care spending account and take the dependent care credit.

Mark: Sounds like a twofer.

Ashley: Well, it’s not a twofer, but because the amounts are so small, and daycare costs are so high, a lot of times …

Mark: You’re speaking from personal experience …

Ashley: Speaking from very personal experience. A lot of times you have enough cost there that it’s in excess of that $5,000, and then the dependent care credit amount, and so that’s something else to look at as well, and that’s one of the very few credits that doesn’t phase out with AGI increases. All that happens with that credit is the percentage of the credit you’re entitled to reduces, but you’re entitled to the credit regardless of what your AGI is.

Mark: You could take the 5,000 dependent care …

Ashley: The pre-tax, correct.

Mark: … the pre-tax, and you could be eligible for this credit.

Ashley: This credit on your tax return, correct.

Mark: You’re saying it doesn’t phase out, or it does phase out?

Ashley: It does not phase out. The credit starts, so it’s $3,000, up to $3,000, for 1 child, 6,000 for 2 or more, and the credit percentage is 35% to as low as 20%.

Mark: That’s a credit to tax?

Ashley: Yes, it’s a dollar for dollar reduction of tax.

Mark: Which is better than a deduction.

Ashley: Deduction, yeah, it’s much better than a deduction.

Mark: I know a little bit about tax. Just …

Ashley: Yeah. That’s good.

Mark: … a little tiny bit.

Ashley: Enough to be dangerous?

Mark: Well, probably. Really dangerous, probably, is how some would say.

Ashley: Yeah, you’d probably have somebody locate your return if you do it yourself.

Mark: Kent Beachy.

Ashley: Oh, OK.

Mark: We’ll put the blame on Kent.

Ashley: That’s good. That’s good.

Mark: Yeah. He might be nervous right now.

Ashley: He probably knows more than you do, right …

Mark: … do, all right …

Ashley: … so I guess it’s better than he’s doing, and not you.

Mark: Right, I just hope that any client that talks to me on classes, taxes, is not listening to this.

Ashley: There you go. Well, you could just say that you get your information from a very good source.

Mark: Who might that be?

Ashley: Me, of course.

Mark: My friend Brad will be nervous right now. Getting back to the tuition stuff, I just … We talked about, sounds complicated.

Ashley: Yes.

Mark: Just being that situation, like the FAFSA form, and there are some other CCC … All these multiple forms, and it just seems to be very, very complicated to me.

Ashley: Families are dealing with a lot when it comes to college. I mean, you’re talking about …

Mark: You have to stress, or I’m going to talk …

Ashley: You talk about the FAFSA, just getting ready, I mean FAFSA forms you have to fill out. Those have nothing to do with the tax piece, but those are … I mean, have everything to do with what you’re paying for school, down to applying, even, the application process, is just such a burden, and so to know that on the back end, you have the opportunity to save even a little bit with these credits is great; but there are lots of moving parts and pieces, and they can get really complicated to make sure, evaluate whether you meet the requirements, and which one would work best for your particular tax situation, and it’s just as complicated to navigate these credits and how you should treat these expenses for tax purposes, as it may be to fill out the FAFSA form.

Mark: That’s a great point. Just speaking from my experience, it’s, you’re excited for your child, you feel nostalgic, “Oh, my … I can’t believe I had somebody graduating. I can’t believe I have somebody going to college,” and you’re going through that stress and that emotion, and where they’re going to go, and the stress and emotion, you want the best for them, and then they’re like, “Oh, you need to fill out this FAFSA form, so that you get whatever scholarship opportunities they might get,” and the stress with that, and then like, “Oh, well, we need to take advantage of these … ” It’s all just very, very stressful. My blood pressure is going up as we’re talking about it.

Ashley: I hear a theme here that … Stress.

Mark: Yes. Yes. Yes.

Ashley: Stress, Mark is very stressed.

Mark: Yes. You got 15 years to figure out how-

Ashley: I think I do, yeah.

Mark: Start counseling now.

Ashley: Right, I know, I know, I think I need to. Yeah, I mean, I think hopefully we can help relieve that stress, or your CPA can help relieve that stress a little bit by guiding you in the right direction, as far as where the tax savings really are, but I think, as we discussed, it starts as early as birth. I mean, setting up these savings accounts, and just having the growth tax-free, and we all know college costs aren’t coming down any time soon, so I kind of look at it as the same as saving for retirement. The earlier you start saving, the more you have, and it’s kind of the same way with college accounts as well, the earlier you save.

Mark: I agree with you. I mean, I would like to think that I was educated in the subject, but I just can never save enough, right?

Ashley: Yeah. Yeah.

Mark: It’s just a struggle, but I would encourage people to save early, and I would encourage people to talk to an advisor.

Ashley: Of course, of course.

Mark: It’s like, “Oh, well, I’ll wait till they’re freshmen in high school.” That’s probably too late.

Ashley: Right.

Mark: You need to be, you know, discussing this earlier.

Ashley: Well, and being a CPA myself, I’m not ashamed to admit that my husband and I reached out to a financial advisor for advice in this area, and he really helped us determine where do you put your money, and, you know, “How much do you have to save, where you put it, where does it make sense,” and I’m happy to say that part of that goes towards a college savings account. Not all of it, but part of it. His good saying is, “You can’t take out loans to fund your retirement, you can’t take out loans to fund college,” so it’s one of those looking up them for advice on what is the happy medium, if I can’t fund my retirement 100%, I can’t fund my college 100%, where do I …

Mark: Correct.

Ashley: Where do I put that it makes the most sense?

Mark: Then guilt the kids into saying, “Okay, you understand I’m doing this when I’m old and decrepit, you won’t take care of me.”

Ashley: Right, right.

Mark: Then get them on video saying, and then …

Ashley: Yes, that’s true.

Mark: … they don’t have an out. That’s my …

Ashley: This is true, yeah.

Mark: That’s my planning strategy.

Ashley: Mark’s girls, did you hear that? You better have a contingency plan in place here. Dad’s counting on you.

Mark: Big time. Very big time. If we talk, you mentioned college cost, and I’m a firm believer that not everybody has to go to college.

Ashley: Right.

Mark: I think there’s plenty of opportunities for people that, but they need to have a plan, right? You just can’t come out of high school and say, “Well, I’m going to become the champion Call of Duty player.” You need to be able to monetize that some way.

Ashley: Right, and there are, some of these, we talked about, there’s a couple different savings accounts that you can open up for college, and one of those options, actually, works for any type of higher education, so it doesn’t have to be an undergraduate degree.

Mark: Like a …

Ashley: It could be a trade school, technical school …

Mark: Great.

Ashley: … something like that, and so-

Mark: That’s just one of the opportunities?

Ashley: Yeah, so one of the savings accounts does, actually, you know, work for that tax-free. Now, it’s important to know, if you put money in the 529, you put too much or the child decides not to go to college, or, you know, that money can come out, it’s just, you’re going to pay taxes on the growth, so …

Mark: It’s just on the growth.

Ashley: Yeah.

Mark: … so you put in $5,000, you take out $6,000, you’re only paying tax on the thousand?

Ashley: Right, because the 5 you put in was after tax dollars.

Mark: It was you money anyway. Well, that seems to be fair, as fair can be, right?

Ashley: Yeah, right, and they’re pretty conservative plans, and so, it’s not going to be too risky, so, I mean, it’s still a good idea to put money there, but you don’t lose it.

Mark: You don’t lose it, right?

Ashley: I guess it’s the good thing; so, and then, one of the credits that we talked about earlier, the lifetime learning credit, you can … That also works towards technical school, trade school, professional education in some instances; and so, that credit can be a good tool, if you’re not even going to college, and if you have, you know, if you’re taking courses for professional education … There may be an opportunity that you could claim that credit.

Mark: Take on that.

Ashley: Mm-hmm (affirmative).

Mark: Well, that’s encouraging.

Ashley: Yeah.

Mark: Because I’m a firm believer that not everybody has to go to college.

Ashley: Right! I agree with that.

Mark: … and that they’re … You need to have a plan, though, right?

Ashley: Mm-hmm (affirmative).

Mark: What’s your plan? What …

Ashley: Right.

Mark: How are you going to get on the pathway to contributing to society, but that might not be through college.

Ashley: Yeah. I agree.

Mark: It might be through something else.

Ashley: Very valid. I agree with that.

Mark: You guys, you talked to your … How old’s your oldest?

Ashley: 6.

Mark: 6 … Have you talked about college?

Ashley: We have a little bit, yes.

Mark: … and were like?

Ashley: You know, my philosophy is that we talk about college as if she doesn’t have a choice to do anything but college, it’s just an extension of high school, and that’s what you do, and so, that’s kind of the way we frame all of our conversations, and, “What do you want to be when you grow up?” and so, right now, we just talk of it in terms of, it’s school. She doesn’t know any different yet.

Mark: Right.

Ashley: … and, you know, myself, growing up, it was the same for me. I never had an option, or never thought of an option less than going to college, but I think it’ll just … It’s a constant conversation, and while I do agree that not everybody has to go to college, it’s not for everybody, I think some type of post-secondary education is required.

Mark: Correct. I agree. Right. Yeah.

Ashley: Yeah, so I think it’s always going to be a conversation, but maybe as they get older, it’ll morph into something different if need be.

Mark: Correct. I hope that by the time your children become college age, or graduated high school, moving on to the next … That there is some leveling out of the expenses.

Ashley: Yeah, that would be great.

Mark: Yeah, it’s just unbelievable, adults coming out of school with, you know, college debt, it’s just a burden, it’s a burden to our … I know that’s not our subject today, we’re talking about, but it’s just unbelievable. Anything that parents or families can do to help people out through taking advantage of credits, are anything like that, is just helpful. It is just unbelievable what these kids could be faced with.

Ashley: Well, on the student loan crisis, so to speak, that we’re having right now is really, it’s a large part of, you know, framing high school kids, and whether or not they’re getting … Go to college, and …

Mark: Right.

Ashley: … one thing that I didn’t mention earlier is that there is a student loan interest deduction.

Mark: I didn’t know about that.

Ashley: We did not talk about that. It’s a $2,500 above-the-line deduction, so it’s a deduction, not a credit; so it reduces your taxable income.

Mark: Which still helps.

Ashley: Yeah, it helps, and the phase-out for that is a little bit higher than some of the other credits, so it doesn’t start to phase out until you hit $130,000 of AGI, so there’s a really good opportunity there for students, you know, coming out of school, that’s, are starting to pay on their loans, to take advantage of that deduction.

Mark: Yeah, I just hope that something happens through the accessibility, the credits, use of the credits, and the deductions that people, you know, whatever their post-high school aspirations be that, you know, that there’s some … If there’s assistance that, take advantage of assistance … That just seems to be very complicated.

Ashley: Well, the government, you know, did make 2 of, some of these credits permanent. They used to be part of the extender package. There’s a lot of talk in the legislation now about, “What are we going to do about college,” the expenses, and so we are seeing some of that movement on the IRS tax side, making some of these permanent, and carving out a part in the code for them; so hopefully …

Mark: Let’s hope it helps.

Ashley: … hopefully, it only gets better from here.

Mark: Yeah, for you.

Ashley: Yeah.

Mark: For you, it’s all about Ashley. Right, before we wrap up, there’s a question we ask every guest.

Ashley: Oh, no.

Mark: You haven’t listened? You don’t know?

Ashley: I know, I haven’t even heard it yet, but if it’s coming from you, I’m sure it’s a doozy.

Mark: If you could have one superpower, what would it be?

Ashley: Oh, goodness. I don’t know if it counts as a superpower, but I would love to have multiple arms, but they would have to be, like, Go Go Gadget arms that move all over the place. Because it would be great to stand somewhere and fold laundry, but then put it away in all 3 kids’ rooms at the same time.

Mark: There you go. I like that.

Ashley: Yeah, so …

Mark: That’s very practical.

Ashley: Yeah, that would be my superpower.

Mark: That sounds awesome, I wish I had that also. Well, that’s our show for today. Thank you for sharing your expertise and experiences there, Ashley. If you’re looking for more business advice that can help your organization, visit www.reacpa.com/podcast, and don’t forget to check us out on iTunes or SoundCloud. Subscribe, rate, and leave a comment. Thank you for listening to unsuitable on Rea Radio. Until next time, I’m Mark Van Benschoten, encouraging you to loosen up your tie and think outside the box.